Latest News

I: General Context

Following the first analysis dedicated to the period from March 1st to March 16, 2026, this note aims to examine the developments during the subsequent period, marked by an intensification of price increases on international markets between March 16 and April 1, 2026.

This sequence is characterized by a significant acceleration of oil product prices, in a context of high volatility, with direct implications on the national market’s supply conditions.

In this context, the Competition Council continued its exchanges with sector operators to assess, in a comparative approach, the dynamics of transmitting variations in international prices to pump prices over the two successive periods.

The analysis aims to complement the initial evaluation by focusing on recent developments from March 16 to April 1, 2026, and their impact on pump prices in the national market.

II: Analysis of the correlation between the variation in international diesel and gasoline prices and their pump prices in Morocco for the period from March 16 to April 1, 2026

Prior to the analysis, it is important to note that the selected prices correspond to refined product prices observed in the North-West European market (NWE), based on transactions in the Amsterdam-Rotterdam-Antwerp (ARA) area, which is the main reference for national operators’ supply.

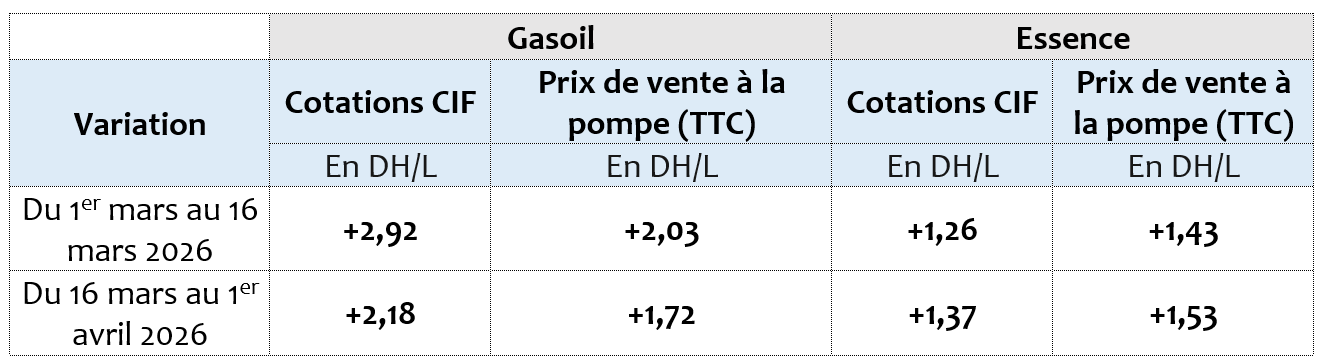

Table No. 1: Variation in CIF prices and pump prices: comparison of the two periods

Source: Based on data provided by the Ministry of Energy Transition and Sustainable Development.

Comparing the variations in CIF prices of refined diesel and gasoline with pump prices reveals significant differences during the period from March 1st to April 1st, 2026, in a context of sustained global price increases.

Diesel

Regarding diesel, the increase in international prices is +2.92 DH/L in the first period from March 1st to March 16, 2026, compared to +2.18 DH/L in the second period from March 16 to April 1, 2026. At the same time, pump prices increase by +2.03 DH/L and then by +1.72 DH/L, respectively.

These changes reflect a partial impact in both cases, with a difference of -0.89 DH/L in the period from March 1st to March 16, 2026 (transmission rate of about 69.5%) and -0.46 DH/L in the period from March 16 to April 1, 2026 (approximately 79%).

Gasoline

As for gasoline, international prices increase by +1.26 DH/L in the first period from March 1st to March 16, 2026, and by +1.37 DH/L in the second period from March 16 to April 1, 2026, while pump prices rise by +1.43 DH/L and +1.53 DH/L, respectively. This results in a more than proportional transmission in both cases, with differences of +0.17 DH/L and +0.16 DH/L.

This situation can be explained by product compensation practices adopted by market operators, involving different modulation of the impact levels between diesel and gasoline. Thus, in a context where the transmission of international diesel price increases remains partial, operators may be encouraged to more strongly reflect the increases in gasoline to partially offset the differences observed in diesel.

However, the extent of this compensation mechanism remains relatively limited, as gasoline represents, on average, only a modest share of operators’ total revenue—around 13%—with diesel playing a significantly predominant role in sales structure.

III: Overall Assessment

As a general conclusion, the comparative analysis of the entire period from March 1st to April 1st, 2026, covering two fortnights, highlights a differentiated impact of international price variations on pump prices in Morocco.

Regarding diesel, the transmission remains partial (total difference of -1.35 DH/L), although an improvement in the transmission rate is observed during the second period from March 16 to April 1, 2026, indicating a reduction in the adjustment gap between international developments and domestic prices.

Regarding gasoline, the transmission appears, in both periods, higher than the variations in international prices, with a total difference of +0.33 DH/L.

These findings highlight the persistence of a certain asymmetry in price transmission mechanisms for different products, in a context of sustained increases in international markets.

In conclusion, the Competition Council did not identify any anti-competitive behavior in the market. However, it emphasizes once again that operators aligning on identical price revision dates, combined with comparable magnitude variations, tend to limit the flexibility of tariff adjustments. This situation can thus hinder the reflection of international price fluctuations and lead to relatively uniform tariff developments among players.

This operating mode partly originates from the old price regulation system, where adjustments traditionally occurred on the 1st and 16th of each month. However, in a now liberalized environment, maintaining this schedule appears increasingly less relevant.

In this context, the Competition Council emphasizes the need to evolve these practices to adapt them to the requirements of a competitive market while considering the necessary market stability. Price-setting decisions would benefit from better integrating the specificities of each operator, particularly by taking into account the actual frequency of supplies, contractual purchasing conditions, stock levels, and implemented commercial strategies.